Early in the COVID-19 pandemic, stay-at-home measures, potential risk of COVID infection at a hospital or doctors’ offices, and concerns over hospital capacity led to sharp declines in health care utilization and spending, including drops in hospital admissions for both acute and elective procedures. There was also a drop in preventive service use. Spending decreased across all health services. While telemedicine use increased rapidly during the pandemic, it did not offset the decrease in in-person care.

Many have wondered whether health care utilization will rebound or even increase to make up for the delayed or forgone care from the past year. If so, this pent-up demand has the potential to increase health spending now or in the coming year.

This brief updates Epic Health Research Network (EHRN) and KFF analysis of data for nearly 10 million admissions in the Epic health record system. Data come from Cosmos, a HIPAA Limited Data Set from Epic customers, which include 250 hospitals across 47 states and 112 million patients. We also used Bureau of Economic Analysis data to look at trends in health services spending. We find that hospital admissions remain below expected levels through early April 2021. Similarly, health spending overall (for hospitals and ambulatory care) remains below expected levels through at least June 2021. Thus far into the pandemic, we have not seen an increase in hospital admissions due to pent-up demand for forgone care in the last year.

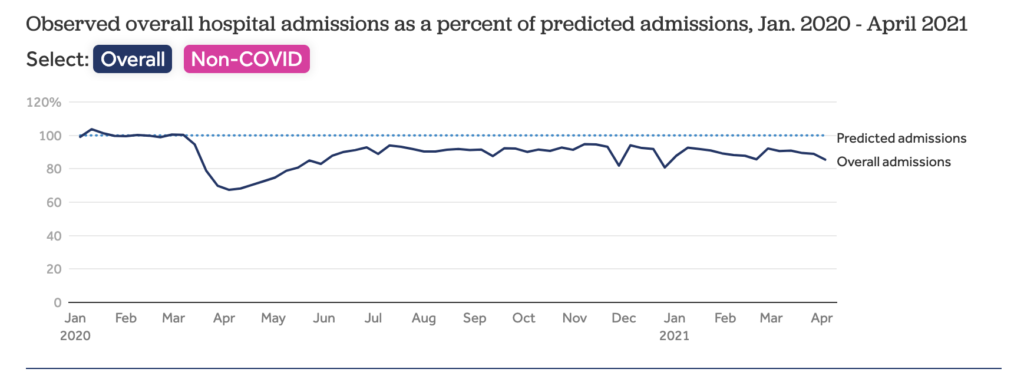

Hospital admissions remained below expected levels through early April 2021

The Epic Health Research Network (EHRN) data show hospital admissions remaining below expected levels through at least April 9, 2021. In the week beginning on April 3, 2021, hospital admissions were 85.5% of what would be expected based on historic patterns. Averaged over the first quarter of 2021, hospital admission rates were 89.4% of what would have been expected in the absence of the pandemic.

Though vaccinations significantly reduced the rates of hospitalizations for COVID-19 in early April 2021 from peak COVID hospitalizations in January 2021, the pandemic is still driving a significant share of hospital admissions. If we remove patients with a COVID-19 diagnosis, we see that all other admissions are 80.7% of expected levels based on pre-pandemic usage in the week of April 3, 2021.

The hospital admissions data in this analysis are only through April 9, 2021. In recent weeks, COVID-19 hospitalizations have begun to trend upward again in part due to the Delta variant. There remains uncertainty about how any future waves of COVID-19 cases might affect hospital utilization more generally.

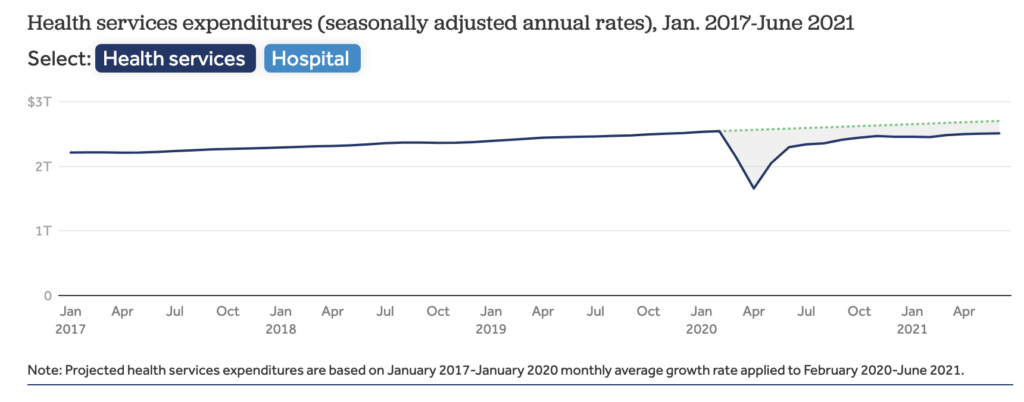

Overall, health services spending is 7.1% below prior years’ trends

Reflecting lower utilization levels, health spending more broadly also remains below pre-pandemic levels. One source for health spending trends is the personal consumption expenditure (PCE) data published monthly from the Bureau of Economic Analysis (BEA). PCE measures the total money spent on health services. Consistent with EHRN, PCE data show spending on health services (hospitals and ambulatory care) remains 7.1% below expected health spending in June 2021 on an annualized seasonally adjusted basis. Spending on hospitals is 4.1% below expected health spending in June 2021. Since January 2021, annualized overall health services and hospital expenditures are growing at a similar rate as prior to the pandemic in 2017-2020.

Missed care could affect providers’ bottom lines and boost insurer profits

While lower levels of utilization have reduced spending, hospitals and other health care providers have qualified for various types of federal assistance during the coronavirus pandemic. Most notably, hospitals and other health care providers received grants from the $178 billion provider relief fund that is being distributed by the Department of Health and Human Services (HHS). Thus, hospitals and providers may be temporarily sustained with the federal assistance. In the long-run once federal assistance dries up, depressed utilization could affect the finances of hospitals and other providers.

Health insurers, in contrast, may be benefiting financially from this decline in hospital admissions and certain other medical services since the start of the pandemic. KFF analysis found that in 2020 average gross margins for health insurers had remained relatively high compared to 2019 and 2018 across the individual market, group market, Medicare Advantage and Medicaid Managed Care markets. In the fully-insured commercial market, the Affordable Care Act requires insurers to return some excess profits to enrollees in the form of rebates.

The implications of missed care for population health remain to be seen

Following an unprecedented decrease in the number of hospital admissions last year, utilization remains below expected levels. The persistence of lower-than-expected utilization suggests some of the care that did not occur early in the COVID-19 pandemic was foregone rather than simply delayed.

Several factors may be contributing to the lower-than-expected number of hospital admissions in early 2021. For example, the economic effects of the pandemic may depress the number of people seeking services. As has been seen in past economic downturns, some people may be forgoing care due to cost reasons.

Suppressed health care use may not be driven only by demand. A more limited supply of health care workers may also lead to continued delays in the availability of care. Health sector employment declined somewhat in the pandemic, and even as health employment rebounds, it may take time for appointment slots to fully reopen.

Even after the pandemic ends, the effects of this delayed and forgone care are yet to be seen. Some of the care that was missed earlier in the pandemic may have been for acute conditions that resolved on their own or chronic conditions that were managed with less service intensity than would have otherwise been delivered. But in other cases, care that was missed may have led to worsened outcomes or even premature death. Looking ahead, people’s experiences with the health care system during the pandemic and increase in telemedicine and alternative ways of delivering care may alter how people use care.

Methods

The analysis is based on EHRN and KFF analysis of the Epic Cosmos Limited Data Set, which includes data for more than 112 million patients from 250 hospitals across 47 states. Contributing organizations were included if they had data through January 1, 2017. Organizations were then excluded if they had go-lives or mergers during the study time period, had multiple weeks of missing data, or showed discrepancies.

Overall, 9.6 million admissions are included in this sample. Expected admissions are based on the historic utilization in the pre-pandemic era. A generalized additive model was trained on weekly admissions data from January 1, 2017 to January 25, 2020 and to generate weekly predicted admissions from January 26, 2020 to April 9, 2021.

Admissions were grouped by week of discharge. COVID-19 admissions are defined as admissions with either a documented COVID-19 diagnosis (U07.01) or other respiratory diagnosis involving a patient who tested positive for COVID-19 or received a COVID-19 diagnosis within 14 days of admission.

The Bureau of Economic Analysis (BEA) data through June 2021 published on July 30, 2021 were used. We used spending data for health services, which does not include spending on pharmaceutical and other medical products. The BEA monthly figures are estimates and are later adjusted using the Quarterly Services Survey. Therefore, there may be some lag in actual spending and monthly BEA estimates of health spending.

Kieran and Jackie are with the Epic Health Research Network (EHRN). Krutika, Matthew, and Cynthia are with KFF.

Early 2021 data show no rebound in health care utilization

Kaiser Family Foundation

August 17, 2021 4:50 pm

Early in the COVID-19 pandemic, stay-at-home measures, potential risk of COVID infection at a hospital or doctors’ offices, and concerns over hospital capacity led to sharp declines in health care utilization and spending, including drops in hospital admissions for both acute and elective procedures. There was also a drop in preventive service use. Spending decreased across all health services. While telemedicine use increased rapidly during the pandemic, it did not offset the decrease in in-person care.

Many have wondered whether health care utilization will rebound or even increase to make up for the delayed or forgone care from the past year. If so, this pent-up demand has the potential to increase health spending now or in the coming year.

This brief updates Epic Health Research Network (EHRN) and KFF analysis of data for nearly 10 million admissions in the Epic health record system. Data come from Cosmos, a HIPAA Limited Data Set from Epic customers, which include 250 hospitals across 47 states and 112 million patients. We also used Bureau of Economic Analysis data to look at trends in health services spending. We find that hospital admissions remain below expected levels through early April 2021. Similarly, health spending overall (for hospitals and ambulatory care) remains below expected levels through at least June 2021. Thus far into the pandemic, we have not seen an increase in hospital admissions due to pent-up demand for forgone care in the last year.

Hospital admissions remained below expected levels through early April 2021

The Epic Health Research Network (EHRN) data show hospital admissions remaining below expected levels through at least April 9, 2021. In the week beginning on April 3, 2021, hospital admissions were 85.5% of what would be expected based on historic patterns. Averaged over the first quarter of 2021, hospital admission rates were 89.4% of what would have been expected in the absence of the pandemic.

Though vaccinations significantly reduced the rates of hospitalizations for COVID-19 in early April 2021 from peak COVID hospitalizations in January 2021, the pandemic is still driving a significant share of hospital admissions. If we remove patients with a COVID-19 diagnosis, we see that all other admissions are 80.7% of expected levels based on pre-pandemic usage in the week of April 3, 2021.

The hospital admissions data in this analysis are only through April 9, 2021. In recent weeks, COVID-19 hospitalizations have begun to trend upward again in part due to the Delta variant. There remains uncertainty about how any future waves of COVID-19 cases might affect hospital utilization more generally.

Overall, health services spending is 7.1% below prior years’ trends

Reflecting lower utilization levels, health spending more broadly also remains below pre-pandemic levels. One source for health spending trends is the personal consumption expenditure (PCE) data published monthly from the Bureau of Economic Analysis (BEA). PCE measures the total money spent on health services. Consistent with EHRN, PCE data show spending on health services (hospitals and ambulatory care) remains 7.1% below expected health spending in June 2021 on an annualized seasonally adjusted basis. Spending on hospitals is 4.1% below expected health spending in June 2021. Since January 2021, annualized overall health services and hospital expenditures are growing at a similar rate as prior to the pandemic in 2017-2020.

Missed care could affect providers’ bottom lines and boost insurer profits

While lower levels of utilization have reduced spending, hospitals and other health care providers have qualified for various types of federal assistance during the coronavirus pandemic. Most notably, hospitals and other health care providers received grants from the $178 billion provider relief fund that is being distributed by the Department of Health and Human Services (HHS). Thus, hospitals and providers may be temporarily sustained with the federal assistance. In the long-run once federal assistance dries up, depressed utilization could affect the finances of hospitals and other providers.

Health insurers, in contrast, may be benefiting financially from this decline in hospital admissions and certain other medical services since the start of the pandemic. KFF analysis found that in 2020 average gross margins for health insurers had remained relatively high compared to 2019 and 2018 across the individual market, group market, Medicare Advantage and Medicaid Managed Care markets. In the fully-insured commercial market, the Affordable Care Act requires insurers to return some excess profits to enrollees in the form of rebates.

The implications of missed care for population health remain to be seen

Following an unprecedented decrease in the number of hospital admissions last year, utilization remains below expected levels. The persistence of lower-than-expected utilization suggests some of the care that did not occur early in the COVID-19 pandemic was foregone rather than simply delayed.

Several factors may be contributing to the lower-than-expected number of hospital admissions in early 2021. For example, the economic effects of the pandemic may depress the number of people seeking services. As has been seen in past economic downturns, some people may be forgoing care due to cost reasons.

Suppressed health care use may not be driven only by demand. A more limited supply of health care workers may also lead to continued delays in the availability of care. Health sector employment declined somewhat in the pandemic, and even as health employment rebounds, it may take time for appointment slots to fully reopen.

Even after the pandemic ends, the effects of this delayed and forgone care are yet to be seen. Some of the care that was missed earlier in the pandemic may have been for acute conditions that resolved on their own or chronic conditions that were managed with less service intensity than would have otherwise been delivered. But in other cases, care that was missed may have led to worsened outcomes or even premature death. Looking ahead, people’s experiences with the health care system during the pandemic and increase in telemedicine and alternative ways of delivering care may alter how people use care.

Methods

The analysis is based on EHRN and KFF analysis of the Epic Cosmos Limited Data Set, which includes data for more than 112 million patients from 250 hospitals across 47 states. Contributing organizations were included if they had data through January 1, 2017. Organizations were then excluded if they had go-lives or mergers during the study time period, had multiple weeks of missing data, or showed discrepancies.

Overall, 9.6 million admissions are included in this sample. Expected admissions are based on the historic utilization in the pre-pandemic era. A generalized additive model was trained on weekly admissions data from January 1, 2017 to January 25, 2020 and to generate weekly predicted admissions from January 26, 2020 to April 9, 2021.

Admissions were grouped by week of discharge. COVID-19 admissions are defined as admissions with either a documented COVID-19 diagnosis (U07.01) or other respiratory diagnosis involving a patient who tested positive for COVID-19 or received a COVID-19 diagnosis within 14 days of admission.

The Bureau of Economic Analysis (BEA) data through June 2021 published on July 30, 2021 were used. We used spending data for health services, which does not include spending on pharmaceutical and other medical products. The BEA monthly figures are estimates and are later adjusted using the Quarterly Services Survey. Therefore, there may be some lag in actual spending and monthly BEA estimates of health spending.

Kieran and Jackie are with the Epic Health Research Network (EHRN). Krutika, Matthew, and Cynthia are with KFF.